Short-Dated Options Show Increased Demand Ahead of NVDA Earnings

Key Points

- NVDA options implied volatility has risen sharply heading into earnings

- Short-dated expirations show the largest increase in demand

- Options markets are pricing greater uncertainty around earnings outcomes

- Traders appear focused on volatility behavior rather than outright direction

Overview

With NVIDIA (NVDA) scheduled to release earnings later this week, activity in the stock’s options market has picked up noticeably. While the underlying share price has remained in a tight range over the past sessions, implied volatility — especially in short-dated expirations — has surged. This pattern suggests that traders are pricing uncertainty and potential price swings around the event, even in the absence of a clear directional bias.

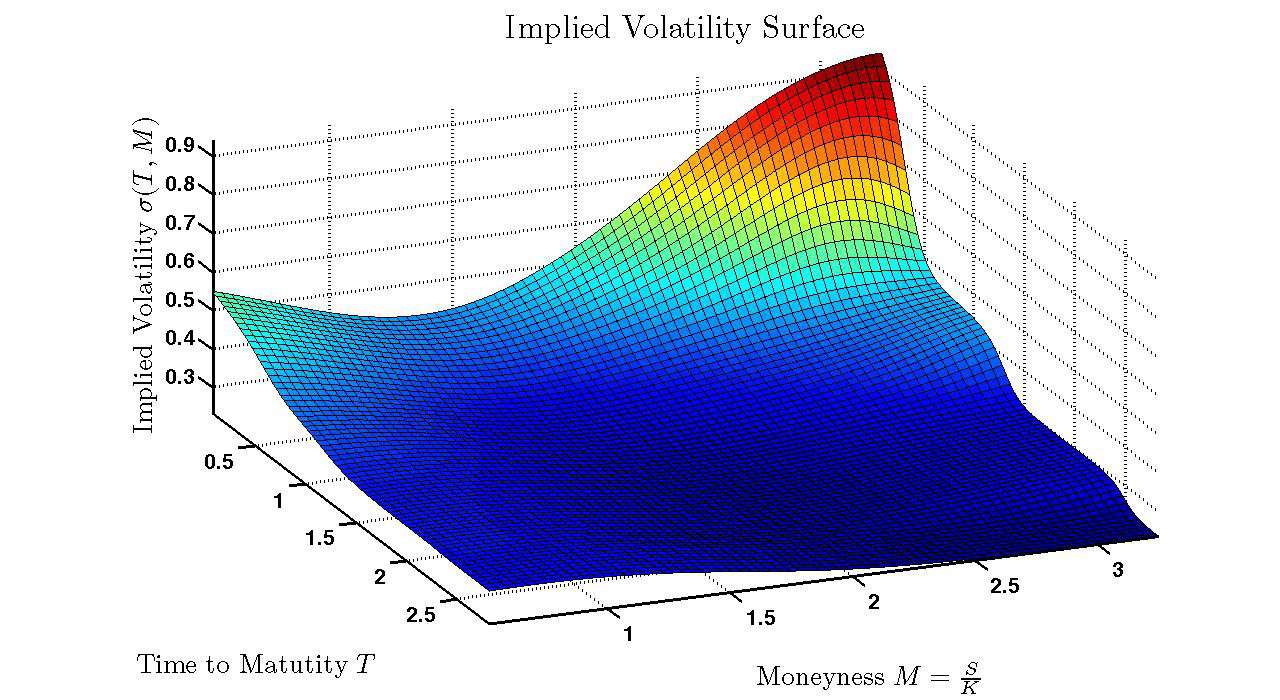

NVDA Implied Volatility Trending Higher

The chart below illustrates how implied volatility has expanded particularly in options expiring within the next week or two. Out-of-the-money and near-the-money short-dated strikes have exhibited the most pronounced increases, signaling heightened demand for event-specific optionality.

Importantly, this rise in implied volatility isn’t mirrored by commensurate increases in realized volatility — indicating that the market is reacting to anticipated risk rather than recent price action.

What Options Markets Are Signaling

When implied volatility climbs sharply before an earnings release, it reflects a market consensus that something could happen — but not necessarily what will happen. Unlike traditional directional moves, this behavior is typical in environments where:

- traders expect wider intraday swings

- market participants are uncertain about the catalyst outcome

- risk premiums are being priced into short expirations

In NVDA’s case, the confluence of earnings expectations, guidance commentary, and potential macro influences has traders assigning a premium to options covering the earnings date.

Interpreting Increased Demand for Short-Dated Options

Short-dated options allow traders to concentrate their exposure around specific catalysts with defined time risk. In the current environment, this manifests as:

- elevated near-term implied volatility

- comparatively smaller moves in longer-dated implied volatility

- heavier positioning in weekly or front-week expirations

This concentration can make risk management particularly important, as theta decay (time decay) and gamma exposure behave differently in tight time windows leading up to an event.

How Traders Might Frame Their Views

IAlthough no one can predict an exact outcome, options traders often think in terms of volatility and relative risk rather than mere direction:

- Neutral/volatility focus

- Some traders may consider structures that benefit if implied volatility contracts after earnings — for example:

- short-strangles or iron condors outside the expected move

- calendar spreads betting on IV decline

- Some traders may consider structures that benefit if implied volatility contracts after earnings — for example:

- Expressive directional exposure

- Others who hold a specific directional view may prefer defined-risk verticals or diagonals that limit downside while still offering asymmetric upside.

- Gamma & time decay nuance

- Traders should be aware that positions with higher gamma and closer expirations can behave unpredictably if the stock gaps sharply after results.

Key Takeaway

The increase in implied volatility — particularly in short-dated NVDA options — reflects uncertainty anchored to the upcoming earnings release, not necessarily strong directional conviction. Options markets are pricing potential volatility first and foremost, which is consistent with historically observed behavior around major events.

Rather than chasing direction, many participants are framing their exposure around volatility expectations, defined risk, and risk management, acknowledging that clarity often comes after the catalyst rather than before.

Looking Ahead

As NVDA approaches earnings, continue watching:

- how implied volatility shifts across expirations

- the divergence between short-dated and longer-dated IV

- real-time realized volatility around price moves

Shifts in these relationships often provide early clues about market expectations and whether post-event reactions align with priced-in risk.